FriMi Digital Bank (Nations Trust Bank, Sri Lanka) | 2018-2019

FriMi Digital Banking

FriMi is Sri Lanka’s first fully digital banking product powered by Nations Trust Bank, built to serve specific socio-economic segments with mobile-first financial services.

What started as a side innovation project inside the bank evolved into a fast-growing fintech brand with 100,000+ active customers within its first year.

I led the strategic repositioning of FriMi from a cashback-driven utility to a trusted digital bank, shifting growth from transactions to behavioral depth.

Scope

- 0→1 digital banking foundation

- Growth evolution from cashback-led utility to value-led fintech

- User lifecycle strategy across Superusers, Churn & Dormant segments

Focus areas

- Product health diagnosis & segmentation

- Behavior-led feature strategy

- Financial confidence reframing

- Embedded research & continuous feedback loops

My role

- Founding Product Designer & UX Strategist

- Built and led the UX function

- Defined product strategy with leadership

- Drove end-to-end design & cross-team alignment

100k+

active customers within first year

200%

increase in average transaction value (6 months)

60%

30-day active user rate

20%MoM

average balance growth (up from <7%)

Problem

A Digital bank without behavioral anchoring

FriMi was acquiring users, but not becoming their bank. Transactions were rising, yet habit formation, stored value trust, and financial identity were missing. The challenge was not feature deficiency. It was behavioral anchoring.

The challenge: How might we transform FriMi from a transactional utility into a trusted financial companion that drives sustained engagement and confidence?

Strategic diagnosis

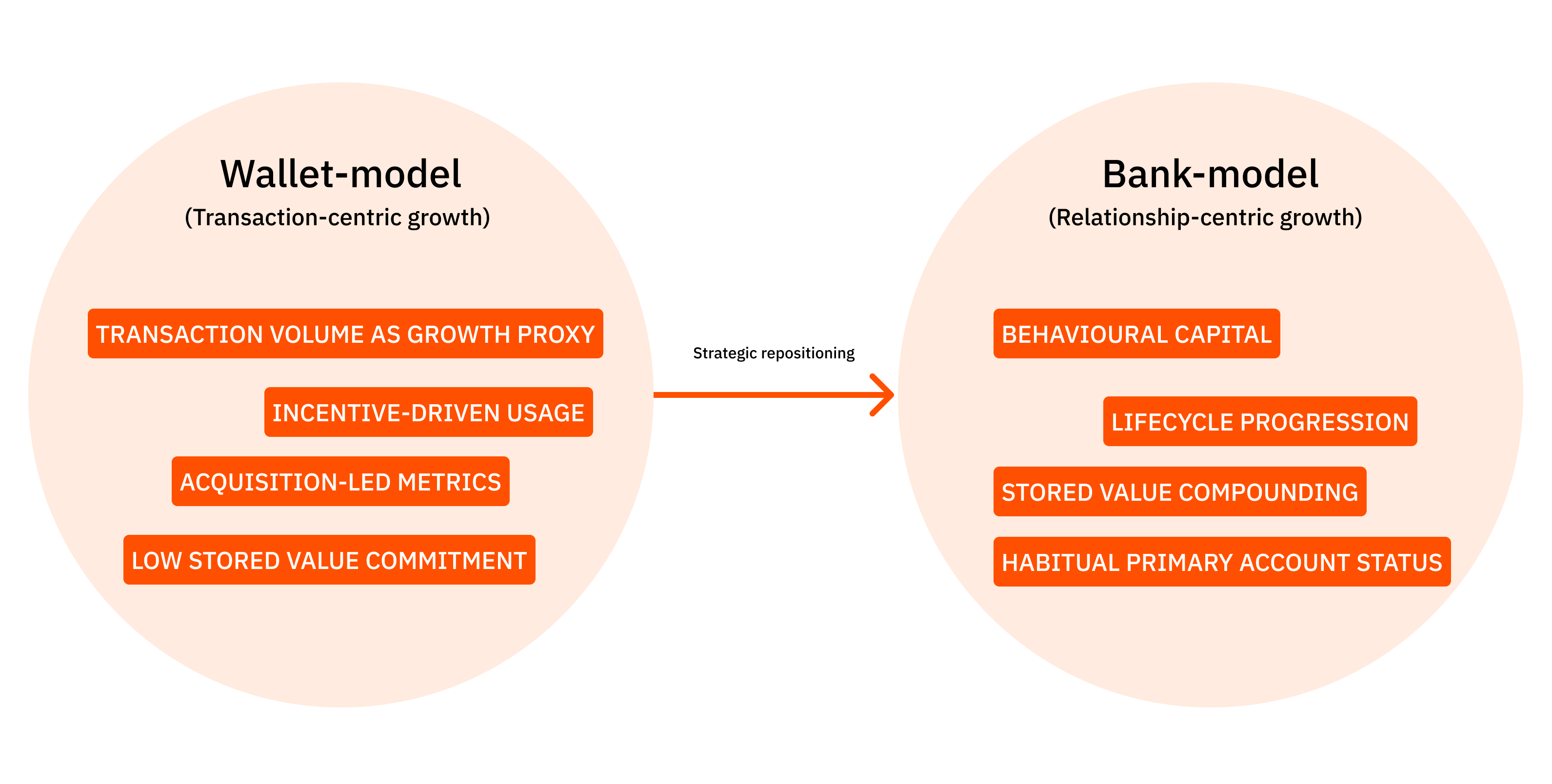

Moving from user counts to behavioral capital

Growth was being measured in downloads and cashback-driven transactions. I reframed executive decision-making around a new question: “How behaviorally invested are our users?” I introduced a lifecycle-based behavioral segmentation model.

The Behavioral maturity model

Instead of demographic segmentation, we defined users by depth of financial engagement

Dormant

Installed but never meaningfully transacted.

Transactional

Using FriMi reactively, mostly for cashback-driven bill payments.

Habitual

Actively transacting, maintaining balance, integrating FriMi into daily life.

This shifted executive decision-making from acquisition metrics to behavioral capital.

We began tracking upward movement between cohorts as a measure of product strength. That reframing alone changed roadmap prioritization

The strategic inflection point

Research revealed a quiet but critical truth:

- 70% of non-transacting users had tried — but failed.

- More than half didn’t know how to add money.

- Over 60% didn’t even realize FriMi was a bank account.

- Those who knew didn’t trust it with meaningful balances.

FriMi was functioning as a wallet. But we were licensed as a bank.

The strategic model

After reframing growth around behavioral maturity, we needed a decision-making framework that ensured we weren’t just increasing activity but increasing meaning.

I introduced the three-layer value model to guide product, brand, and roadmap decisions. We adopted a simple rule: initiatives had to contribute beyond baseline utility toward emotional or social value or they did not make the roadmap.

Functional

Baseline banking reliability

Emotional

Confidence, independence, reduced anxiety

Social

Aspirational identity, legitimacy, belonging

Top strategic moves

- Institutionalizing trust from the first interaction

Trust failure was not a usability issue, but a legitimacy gap. Users did not perceive FriMi as a bank. Without early institutional clarity, stored value behavior would never emerge.

What We Changed

- Repositioned onboarding from feature introduction to institutional framing

- Clarified regulatory identity (bank account, not wallet)

- Reduced ambiguity in top-up and KYC flows

- Embedded contextual reassurance at trust-sensitive moments

- Simplified the “first money in” experience to accelerate commitment

Impact

- Onboarding completion and first-deposit conversion increased significantly.

- Drop-offs reduced in onboarding

- Reasserting banking legitimacy over incentive dependency

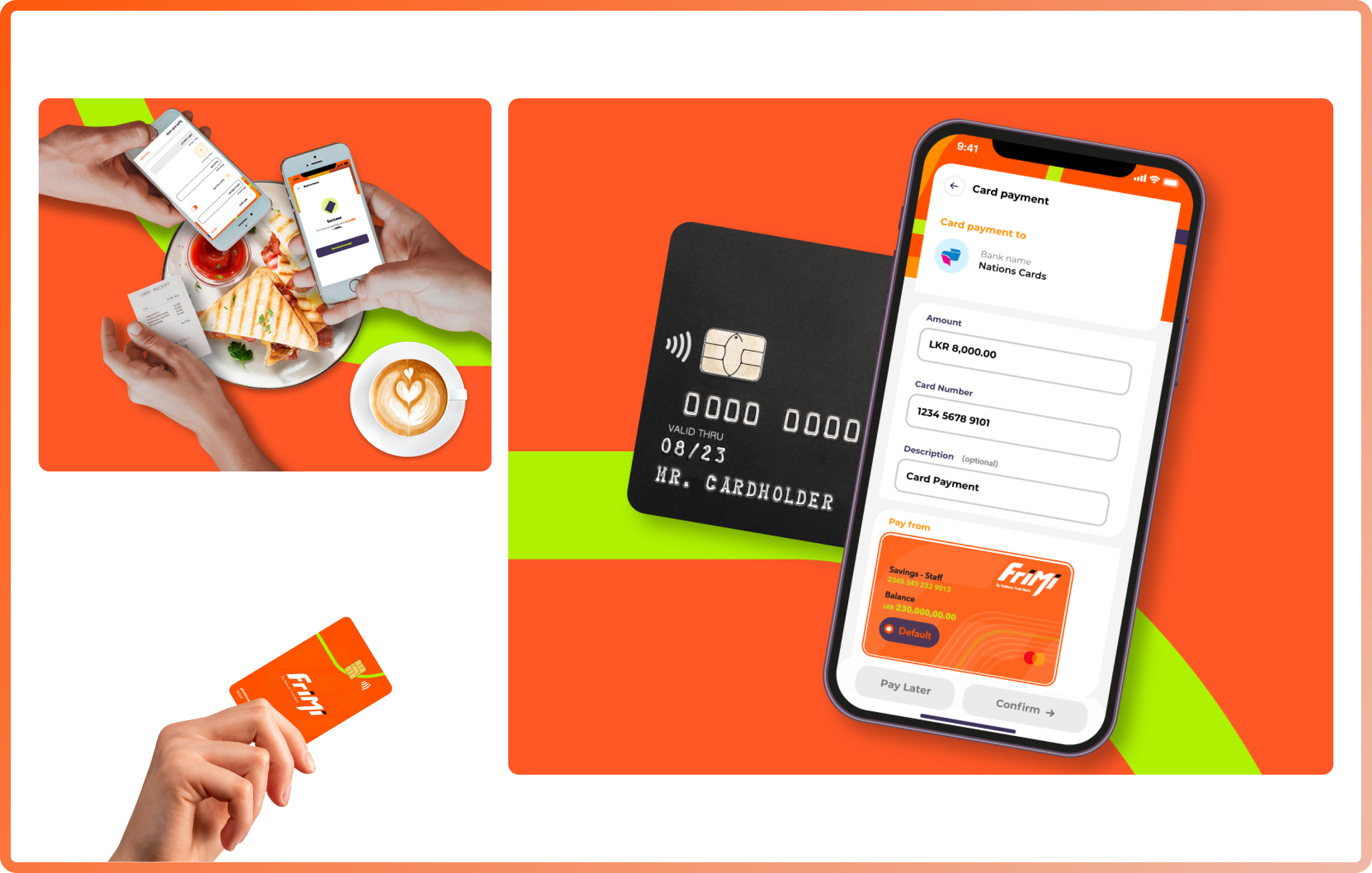

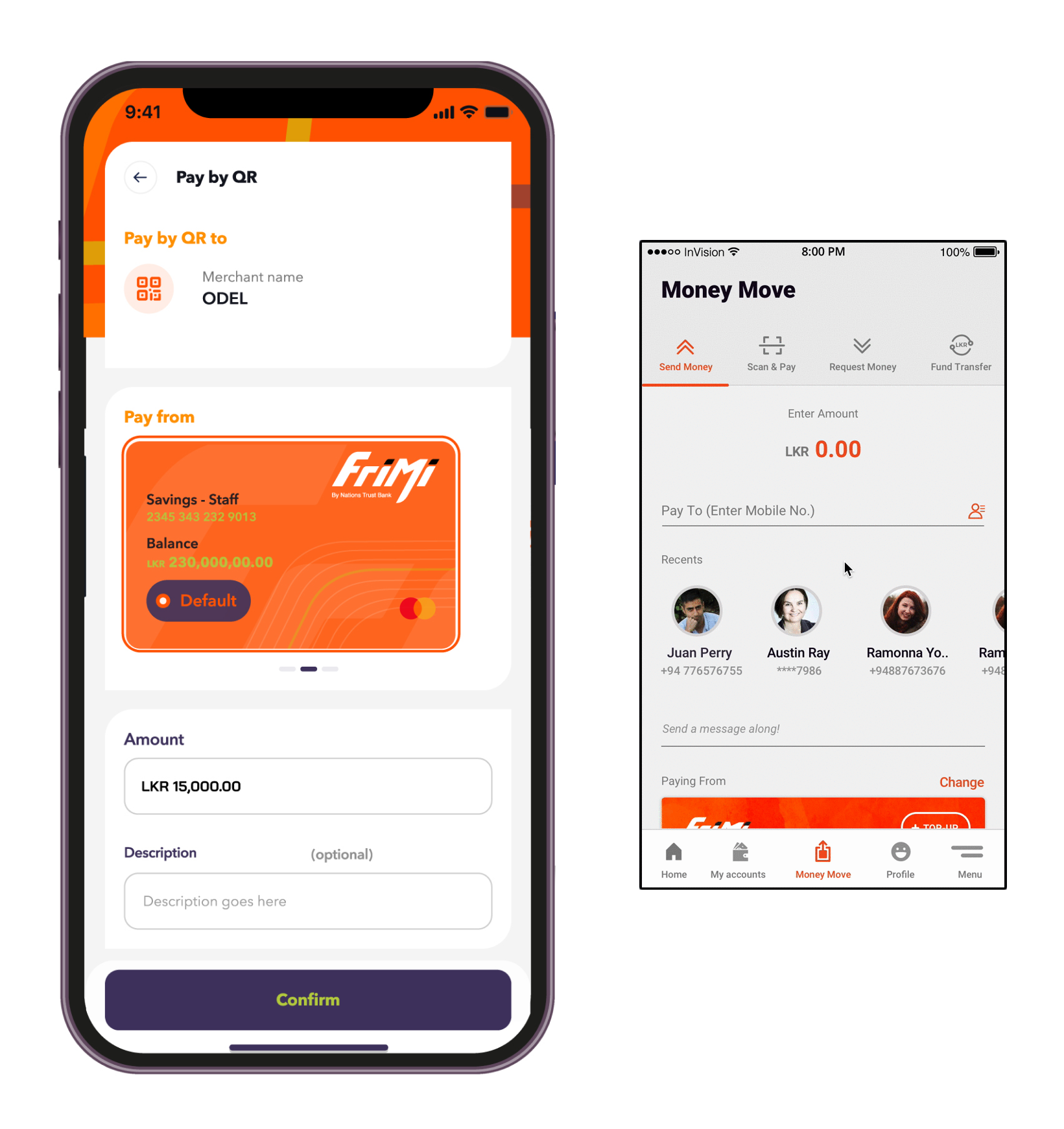

Cashback was driving transactions, but not trust. Users treated FriMi as a reactive payment tool. We needed to shift perception from “use when incentivized” to “this is my account.”

What We Changed

- Elevated balance and account state as the dominant visual anchor

- Reduced promotional hierarchy that distorted perceived value

- Re-centered transactions, statements, and controls as core banking behaviors

- Strengthened financial language across flows to reinforce institutional identity

- Repositioned bill payments as part of account management, not reward mechanics

Impact

- +200% average transaction value

- Balance growth from <7% → 20% MoM

- 60% became 30-day active

- Making financial confidence legible

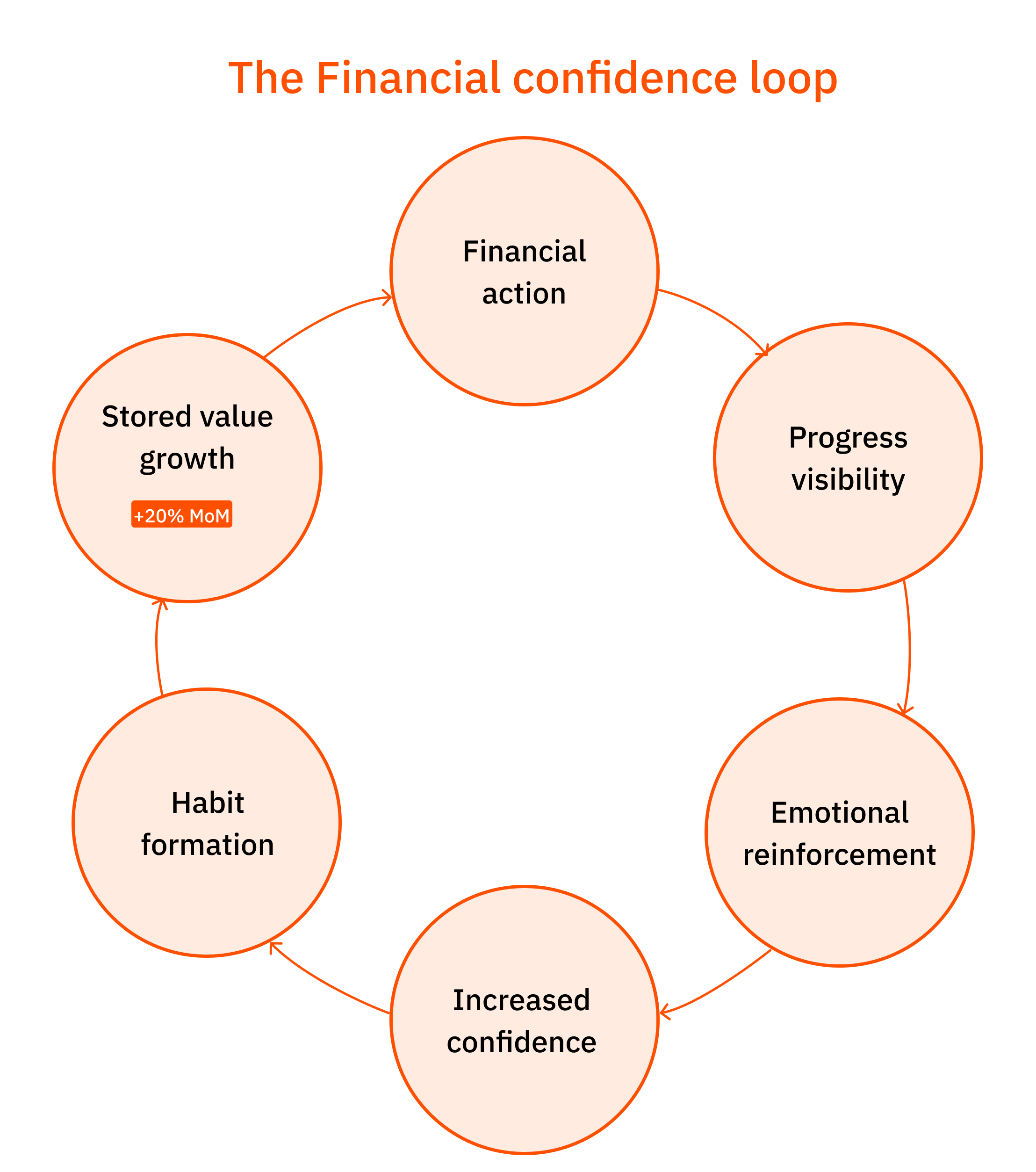

Banking with FriMi felt functional, but not empowering. Users were transacting, but not building confidence.To become a primary financial account, progress had to be visible. Hence, I introduced a behavioral reinforcement system designed to convert actions into confidence.

What We Changed

- Made financial progress legible, not abstract

- Turned usage data into personal narratives

- Designed reinforcement moments after key actions

- Reduced friction in recurring financial behaviors

- Anchored savings growth as visible momentum

Impact

- +20% month-over-month balance growth (up from <7%)

- 60% of users became 30-day active

- Increased stored value retention across cohorts

- Higher repeat transaction frequency per active user

This shifted growth from transactional volume to compounding financial confidence.

FriMi Digital Bank (Nations Trust Bank, Sri Lanka) | 2018-2019

FriMi Digital Banking

FriMi is Sri Lanka’s first fully digital banking product powered by Nations Trust Bank, built to serve specific socio-economic segments with mobile-first financial services.

What started as a side innovation project inside the bank evolved into a fast-growing fintech brand with 100,000+ active customers within its first year.

I led the strategic repositioning of FriMi from a cashback-driven utility to a trusted digital bank, shifting growth from transactions to behavioral depth.

Scope

- 0→1 digital banking foundation

- Growth evolution from cashback-led utility to value-led fintech

- User lifecycle strategy across Superusers, Churn & Dormant segments

Focus areas

- Product health diagnosis & segmentation

- Behavior-led feature strategy

- Financial confidence reframing

- Embedded research & continuous feedback loops

My role

- Founding Product Designer & UX Strategist

- Built and led the UX function

- Defined product strategy with leadership

- Drove end-to-end design & cross-team alignment

100k+

active customers within first year

200%

increase in average transaction value (6 months)

60%

30-day active user rate

20%MoM

average balance growth (up from <7%)

Problem

A Digital bank without behavioral anchoring

FriMi was acquiring users, but not becoming their bank. Transactions were rising, yet habit formation, stored value trust, and financial identity were missing. The challenge was not feature deficiency. It was behavioral anchoring.

The challenge: How might we transform FriMi from a transactional utility into a trusted financial companion that drives sustained engagement and confidence?

Strategic diagnosis

Moving from user counts to behavioral capital

Growth was being measured in downloads and cashback-driven transactions. I reframed executive decision-making around a new question: “How behaviorally invested are our users?” I introduced a lifecycle-based behavioral segmentation model.

The Behavioral maturity model

Instead of demographic segmentation, we defined users by depth of financial engagement

Dormant

Installed but never meaningfully transacted.

Transactional

Using FriMi reactively, mostly for cashback-driven bill payments.

Habitual

Actively transacting, maintaining balance, integrating FriMi into daily life.

This shifted executive decision-making from acquisition metrics to behavioral capital.

We began tracking upward movement between cohorts as a measure of product strength. That reframing alone changed roadmap prioritization

The strategic inflection point

Research revealed a quiet but critical truth:

- 70% of non-transacting users had tried — but failed.

- More than half didn’t know how to add money.

- Over 60% didn’t even realize FriMi was a bank account.

- Those who knew didn’t trust it with meaningful balances.

FriMi was functioning as a wallet. But we were licensed as a bank.

The strategic model

After reframing growth around behavioral maturity, we needed a decision-making framework that ensured we weren’t just increasing activity but increasing meaning.

I introduced the three-layer value model to guide product, brand, and roadmap decisions. We adopted a simple rule: initiatives had to contribute beyond baseline utility toward emotional or social value or they did not make the roadmap.

Functional

Baseline banking reliability

Emotional

Confidence, independence, reduced anxiety

Social

Aspirational identity, legitimacy, belonging

Top strategic moves

- Institutionalizing trust from the first interaction

Trust failure was not a usability issue, but a legitimacy gap. Users did not perceive FriMi as a bank. Without early institutional clarity, stored value behavior would never emerge.

What We Changed

- Repositioned onboarding from feature introduction to institutional framing

- Clarified regulatory identity (bank account, not wallet)

- Reduced ambiguity in top-up and KYC flows

- Embedded contextual reassurance at trust-sensitive moments

- Simplified the “first money in” experience to accelerate commitment

Impact

- Onboarding completion and first-deposit conversion increased significantly.

- Drop-offs reduced in onboarding

- Reasserting banking legitimacy over incentive dependency

Cashback was driving transactions, but not trust. Users treated FriMi as a reactive payment tool. We needed to shift perception from “use when incentivized” to “this is my account.”

What We Changed

- Elevated balance and account state as the dominant visual anchor

- Reduced promotional hierarchy that distorted perceived value

- Re-centered transactions, statements, and controls as core banking behaviors

- Strengthened financial language across flows to reinforce institutional identity

- Repositioned bill payments as part of account management, not reward mechanics

Impact

- +200% average transaction value

- Balance growth from <7% → 20% MoM

- 60% became 30-day active

- Making financial confidence legible

Banking with FriMi felt functional, but not empowering. Users were transacting, but not building confidence.To become a primary financial account, progress had to be visible. Hence, I introduced a behavioral reinforcement system designed to convert actions into confidence.

What We Changed

- Made financial progress legible, not abstract

- Turned usage data into personal narratives

- Designed reinforcement moments after key actions

- Reduced friction in recurring financial behaviors

- Anchored savings growth as visible momentum

Impact

- +20% month-over-month balance growth (up from <7%)

- 60% of users became 30-day active

- Increased stored value retention across cohorts

- Higher repeat transaction frequency per active user

This shifted growth from transactional volume to compounding financial confidence.